Stitch Fix's Long Thread

Why Stitch Fix might be an overnight success, decades in the making.

Welcome to The Flywheel, where we take a deep look at a company’s business and products to understand which areas are spinning smoothly and where a little grease may be needed. If you’re reading this but haven’t subscribed, click below to join 600+ of your smartest friends and peers.

If you liked this post, please click like and share with your friends! Onto the article.

[Full disclosure: I own a modest amount of SFIX shares.]

In previous editions of The Flywheel, I’ve told the story of companies—Peloton, Zoom, Robinhood—that are experiencing runaway growth. Pandemic fueled growth, perhaps, but growth nonetheless. Those companies had a smooth flywheel already established, and when the pandemic hit it spun into overdrive. Today’s company, Stitch Fix, is a different sort of story.

Stitch Fix has struggled since the pandemic started. As people have stopped leaving their homes, demand for new clothing—and in particular non-pajama..I mean athleisure, clothing—has dried up. In the 3rd quarter of the most recent fiscal year (April-June 2020) revenue decreased for the first time ever, compared both to the immediately preceding quarter and the same quarter in the previous year.

And yet the company has an interesting Flywheel that I believe bodes very well for the company and any of its shareholders who have the patience to let it play out. Let’s dig into the details.

What is Stitch Fix

Stitch Fix is an online clothing store that takes a unique approach to helping its customers (or ‘clients’) find clothing. Unlike other online clothing stores that attempt to mimic the in-person shopping experience, Stitch Fix does not invite customers to browse for items and order anything they wish. Instead, Stitch Fix’s service is built entirely around its personal stylist services.

The customer journey begins with the ‘Style Profile’ quiz: a series of questions about fit, style, color, and price preferences that help Stitch Fix’s stylists (with an algorithmic assist) pick out the customer’s first ‘Fix’. A Fix is a box with 5-7 pieces of clothing and accessories, sent to the customer’s home where they have 3 days to try the items on and ‘check out’. Stitch Fix charges customers a $20 styling fee per Fix, but credits it back against any clothing purchases.

The check out process is where the customer (1) returns the items they didn’t like, and (2) leaves detailed feedback on all items (whether they kept them or not). Stitch Fix uses this feedback to better understand the customer’s preferences, enabling them to improve the quality of their picks over time.

This feedback loop is Stitch Fix’s core capability, and the company has invested heavily in data science to improve it over time. The company’s blog has an extremely detailed overview of the algorithms it uses to satisfy customer requests full of cute graphics such as this one:

At Stitch Fix, data science is the product, and it just so happens to be applied to making clothing recommendations. CEO Katrina Lake has said “data science isn’t woven into our culture; it is our culture”.

Why Stitch Fix

As anyone who likes clothing but doesn’t particularly enjoy shopping will attest, the promise of Stitch Fix is alluring. The idea that a stylist will hand choose the perfect clothing for me and that I will never need to think about what to buy (and maybe someday, what to wear) seems magical.

Unfortunately reality doesn’t always match up with magic. Or at least it didn’t for me. After trying Stitch Fix unsuccessfully several times, I realized the company was caught in a true chicken-and-egg scenario. To make good recommendations, you need customers who are willing to put in a certain amount of work (filling out the style profile and persevering through multiple mediocre Fixes). And without good recommendations, how will you convince customers to go through the effort to get over the hump?

I wanted to understand if and how Stitch Fix can solve its chicken-and-egg problem and, if so, what it might mean for the company’s outlook.

Stitch Fix’s Flywheel

Style Profile

The flywheel starts when a customer fills out a style profile. This is a prerequisite for starting as a Stitch Fix customer. The more thoughtfully a customer fills out their profile, the more likely it is they will enjoy their first Fix.

First Fix Success

A customer’s first interaction with every company is critical, and this is especially true for Stitch Fix. The first Fix is when a customer sees if the effort they put into their style profile was worth it. Based on the success of this interaction, customers are either going to churn or give Stitch Fix another chance.

Stitch Fix tracks the quality of their recommendations with a metric called ‘Success Rate’. This is the percentage of items that customers keep upon checking out. If I receive 5 items in my box and keep 2, that’s a 40% success rate.

One could confidently speculate that customers whose first Fix success rate is at or near 0 never come back, while those closer to the opposite extreme enter what I’ll call the single player flywheel.

Single Player Flywheel

In the single player flywheel, each individual customer is enjoying a virtuous cycle of ever improving recommendations. Consider the following metrics from Stitch Fix’s 2019 annual shareholder letter:

This shows that as a customer proceeds from the first Fix to their third, their success rate increases (100% is the indexed value for the first Fix. The company does not publish actual success rates); in 2018, that increase was by 14%. This is what you’d hope for: as a customer provides more data to Stitch Fix, the company is able to improve its recommendations.

In addition to improving Fix success, Stitch Fix recently started selling individual items as part of the single player flywheel. At first it was accessories that complement items in the Fix, and more recently they have added a ‘shop’ section that allows customers to choose among a small, curated selection of items. The implication of this is that Stitch Fix no longer needs to rely solely on Fixes to get feedback on recommendations.

Margin

As the company has more and more customers spinning the single player flywheel, the company accrues several financial advantages. This Forbes article does a nice job breaking down the ways in which the company’s unique datasets provide operations, inventory management, and other efficiencies.

This makes logical sense: the company only suggests a small number of total SKUs to customers, and over time it becomes increasingly confident in its decisions. That means from everything from designing to buying to warehousing to selling, Stitch Fix has the ability to make smarter decisions when it comes to the financial risk associated with clothing compared to everyone else.

Perhaps most intriguing is Stitch Fix’s ability to use its ever-increasing understanding of its clients’ preferences in the clothing design process. Stitch Fix has a unique ability to identify merchandising gaps and can design clothing in-house to meet those gaps.

The Dotted Lines

If the Flywheel ended there, then it wouldn’t really be a flywheel. After all, there’s nothing feeding back into the beginning. Customers may be experiencing a great single player flywheel, but from a company perspective, the beginning of the flywheel isn’t being spun by later activities. That would mean that there’s nothing unique about Stitch Fix’s ability to acquire customers. It has to acquire customers in the same boring and expensive way everyone else does: social media ads and referrals.

Going back to our chicken-and-egg problem, if Stitch Fix’s data science machine wasn’t making it easier for new clients to get over the initial hump, it would be hard to believe that Stitch Fix has a bright future.

At first glance, this is precisely what I thought the Stitch Fix story was, and it was the story I saw when I looked at the active customer metrics reported by the company:

Even before COVID, Stitch Fix’s active client base was growing, but that growth was slowing down (the grey line). And yet, the revenue per active customer (the green line) was growing nicely, with accelerating growth (the blue line) up until COVID.

But then I saw something that changed my mind. Remember the data on how customers Fix success improved as they went from the 1st Fix to the 3rd? Here’s what that chart looks like if we add in 2019 data as well:

This says that relative to customers’ first Fixes in 2018, first Fixes sent in 2019 had a 17% higher success rate. This may seem insignificant, but it actually changes everything. This data point allows us to connect the flywheel back to the beginning and draw the two dotted lines:

Improved First Fix Success

A Fix success rate that is improving over time proves that the single player flywheel bleeds outwards to the company’s overall flywheel. That means that the more data the company collects about customers the better recommendations it can make not only to that individual customer, but also to every new customer. This is important because now the company has a new unique string in its customer acquisition bow.

Customer Acquisition Model

If Stitch Fix had confidence that the average new customer would love their first Fix and therefore enter the single player flywheel, how much would Stitch Fix pay to acquire this average customer? Potentially an unlimited amount.

Today, this is not the case. Stitch Fix needs to be very prudent and risk-averse with its customer acquisition costs because too many new customers are churning after a small number of low-success Fixes. But in the future? Stitch Fix’s entire trajectory could change.

When that day comes, Stitch Fix can try all sorts of levers to grow the top of its funnel. Today, Fixes have a $20 styling fee. Maybe in the future the first 5 Fixes are free. Or maybe in the future customers get a $100 credit for filling out their style profile. Options abound for companies that can retain users and grow their spend over the course of years.

What Kind of Company is Stitch Fix?

Aggregator or Normal Company?

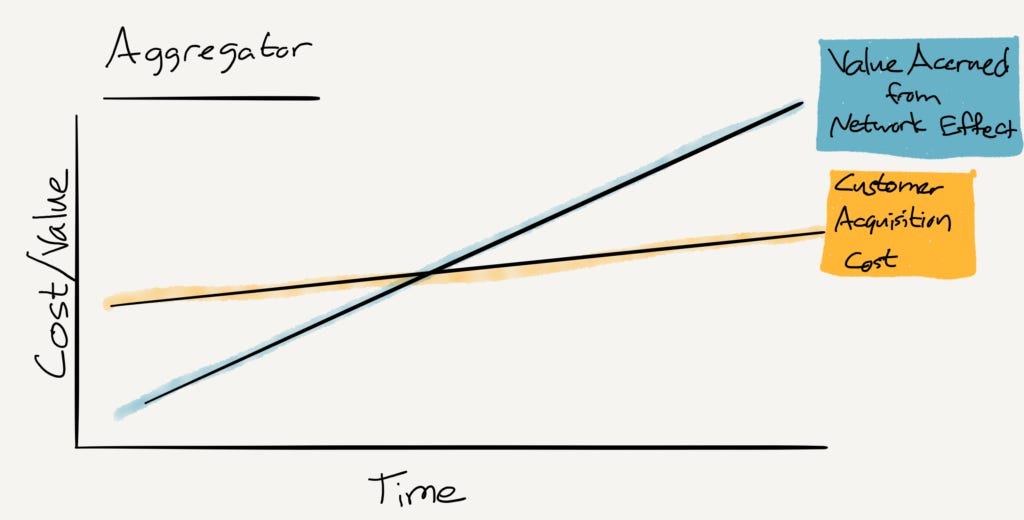

Ben Thompson wrote about Stitch Fix in 2017 right before their IPO. Back then, he contrasted Stitch Fix with other high flying, network effect companies who—rightly—spend aggressively to acquire customers because their lifetime value (which includes all the other customers they will attract) was likely to be even higher than the cost. These companies are aggregators (graphics are from Ben’s excellent blog Stratechery):

Stitch Fix, in contrast to these hugely unprofitable, high growth companies, was growing modestly (30% YoY qualifies as modest in this landscape) and, crucially, was already profitable at IPO.

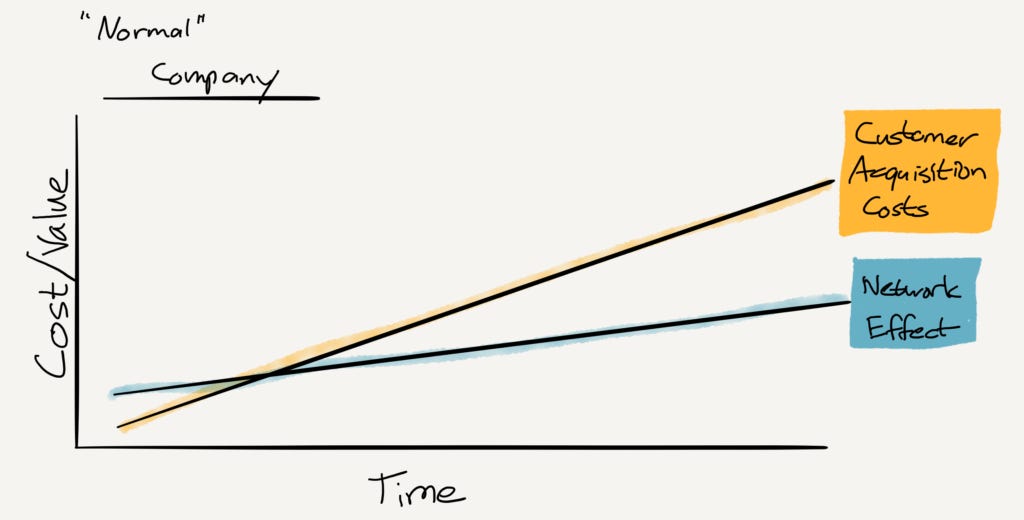

This made Stitch Fix something of a rarity, and Thompson’s takeaway was that it was important to prove that you can still build a boring, normal company. Thompson credited Katrina Lake’s maturity and prudence in identifying that Stitch Fix is not a network effects aggregator and therefore that they must acquire customers in a way that allows the company to be short term profitable. Again, graphic from Stratechery:

A Third Option

Stitch Fix may yet prove to be a third type of company, which we can call a not-yet aggregator. A not-yet aggregator looks like a ‘normal company’ today, but the crucial difference is that their network effect line isn’t actually linear. It just looks linear today. With a long enough time frame, a not-yet aggregator looks like this:

If true, then Stitch Fix is heading toward a tipping point. When its ability to recommend clothing to new customers improves past a certain point, Stitch Fix can and will flip a customer acquisition switch. And with the command of costs that Thompson rightly credits the management team for, it would be surprising if they didn’t.

The question is where that tipping point is. Does success rate need to be 2x better than it is today, or 10x? The precise number is anyone’s guess, but I’d venture to say we have a while before Stitch Fix gets there.

Outlook

So what kind of company is Stitch Fix? In a world that loves to glorify long-term thinking after the fact but tends to reward short termism in the present moment, Stitch Fix seems underappreciated. Yes, growth today has slowed, but if the observations I have made are accurate, then Stitch Fix is slowly building a force to be reckoned with. Even 10-20% improvements can compound powerfully over the span of years or decades. In 2030, how might we be talking about Stitch Fix if they can keep the steady progress alive?

Of course there are risks. There are always new competitors popping up in this market, and apparel is a famously fickle industry. But it’s hard to imagine other apparel companies being more resilient in the face of change than Stitch Fix, who now have nearly a decade of experience processing large amounts of direct feedback, straight from customers. This data advantage is real and it compounds every day. Who will be able to identify changing trends faster than Stitch Fix?

Perhaps, then, the only real existential risk is that the team gets, well, bored. Long-term thinking is hard, patience is a rare virtue, and if revenues, profits, and the stock price grow too slowly, it may be hard for the company to keep hold of the talent it will take to get them there.

If they can find a way, don’t be surprised to see Stitch Fix sneak up on some people in 5-10 years. But not you, because you read The Flywheel.

That’s it for this edition of The Flywheel. Thanks so much for reading. A huge thanks to Tanya, Lea, Nate, Carolina, Brittany, Seth, Anant, and Dan for proof reading and editing.

If you liked this article, please subscribe and share with a friend!

What’s your take on Stitch Fix? Feel free to share you thoughts with me on Twitter here.

Great breakdown of one of my favourite companies. Subbed!