Zoom's Meteoric Rise

How Zoom became the default video chat option and how it can stay that way

Welcome to The Flywheel, where we take a look at a company’s product portfolio to understand which areas of the business are spinning smoothly and where a little grease may be needed. Learn more about The Flywheel here.

If you’re reading this but are not subscribed, consider joining us to receive every new Flywheel article (1-2 times per month) directly in your inbox!

Introduction

When COVID hit the US full force in March and live events started to shut down, Zoom entered all of our lives in a major way. Suddenly school was virtual, work was from home, workouts were online, and even weddings and funerals were performed at a distance. And somehow it was Zoom—of all video chat products—that became the default option, seemingly out of the clear blue sky.

Earlier this week we witnessed just how well being the default option has translated into business results for Zoom. On Monday the company released its earnings from Q2, its first full COVID-quarter. Pick a metric (financial or user) and it was likely up several hundred percentage points. Revenue grew 355%, net income increased 35-fold, both year-on-year, and there are similarly huge numbers on the user side.

The market, of course, ate up these results. On Tuesday Zoom ($ZM) shot up almost 40%. In one day. Even after giving back most of these gains later in the week, ZM was still up over 1,000% since its IPO just 17 months ago, and has a market cap over $100B. The rewards to being the default option have been staggering for Zoom shareholders.

In this post I will explore how and why this happened. In a world where there's nothing to do but have a video conference, how did this plucky upstart become the winner (at least to this point) of what was an already crowded and competitive market? And if we understand this a bit better, are there lessons we can learn about Zoom's forward looking prospects?

Product and Company Overview

I want to start with a brief overview of Zoom's product and history. I know, we all use Zoom every day, so I won't get too deep into the basic facts. But there are a couple of notable highlights.

It Just Works

First, the product just works. And believe me, I really, truly didn't want to use this phrase. I have had lots of conversations with friends over the past few months speculating on why Zoom has been so successful, and 'it just works' or 'Skype sucks' is generally as far as the conversation goes.

But unsatisfying as it may be, this is the inescapable key behind Zoom's meteoric rise. And while I'm not qualified to give a technical breakdown of why Zoom's product is more reliable than Google's, what's extremely clear is that it is not random luck.

Eric Yuan (Zoom's CEO) is a deep video conferencing expert who had close to a decade of experience working on video conference tools at Webex before starting Zoom. Webex eventually became part of Cisco, and Yuan had attempted to pitch what became Zoom in 2011. His proposal was rejected, so he left to start the company.

One of the best, most experienced technical video conference people in the world has been obsessing nonstop on building the best video conference tool fit for the modern world since 2011. Contrast this to competitors like Google and Cisco and Microsoft—who have probably had one or two teams focused on it as a non-core part of their business model—and it suddenly makes more sense that Zoom ‘just works’, while the others..not so much.

A video conference by definition has multiple people on it, and therefore each video chat is a de facto product demo for the software. Which means that if it works well and everyone is happy, it's a big boost for the product. If you then go onto a Google Hangout and have some funky issues, the odds are decent that someone will suggest using Zoom.

No Download or Account Required

The 2nd piece to highlight is that Zoom was and is simpler to adopt than competitors. This may sound simple but it's the lubricant on the flywheel. If someone sends me a calendar invite and wants me to use a tool like BlueJeans that requires me to download some nonsense or Skype where I need to remember my password from 10 years ago, I am likely to ask for an alternative. If someone sends me a Zoom link, there's no legitimate reason why I cannot at least try it. It's as easy as clicking a link.

These two factors combined help explain why Zoom was winning the video conference war, well before COVID. This excerpt from Forbes profile of Yuan in April 2019 describes the product superiority even as far back as 2013, when it first launched:

When Zoom launched, it had several key differences from the crowd. Its lightweight Web client could figure out almost instantly what kind of device you were using, meaning Zoom didn’t need different versions for Mac or PC. It also provided a software layer that shielded any bugs that might be introduced when a browser like Chrome, Firefox or Safari pushed an update. Zoom could operate even at 40% data loss, so it would still work on a spotty or slow internet connection. And at $9.99 per host per month ($14.99 today), it undercut its rivals. Zoom customer service chief Jim Mercer was then working at competitor GoToMeeting when a colleague opened a Zoom account to see what the hype was about. “One click, we were in, and there were 25 feeds of participants at the same time,” he says. “We were like, ‘What is this voodoo? How are they doing it?’ ”

Zoom’s Flywheel

With this background in mind, let's examine the Zoom flywheel a bit more closely. Now is a good time to introduce the idea of Flywheel Types. Max Olson has a good primer on 6 major types of Flywheels. I won't talk about all of them in this post, but Zoom's flywheel is an interesting combination of what he calls the Network Effects and the Proprietary Tech flywheels. Both flywheels are powerful yet vulnerable for Zoom, as I'll explain:

The Network Effect Flywheel

It all starts with one successful, delightfully simple video call. It just works, and after it just works, you inexplicably love the product. Perhaps because most of us have years of baggage of 'I can hear you but I can't see you' and 'hmmm no not yet', a simple, delightful experience is more powerful than you might logically expect it to be.

Since every video call is a product demo the company doesn’t have to pay for, more successful calls leads to more users, leads to more successful calls, leads to more users...etc.

The Proprietary Tech Flywheel

There's something else going on too, in addition to the relatively straightforward user flywheel. The Zoom advantage is that the tech just works. In addition to the reasons already discussed, a lot of it has to do with the fact that it works on all devices, in every setting, no matter what. The more Zoom grows its users, the more edge cases it learns how to handle, and it has the cash available to invest in the infrastructure to support those use cases.

Not only that, but Zoom can then also add additional use cases. Webinars and larger conferences? Sure why not, we already have the ability to run a regular meetings for up to 1000 people without a hitch. Both of these investments (into the infrastructure to handle the edge cases and the new customer facing use cases) feed back to the start of the flywheel. More successful calls, feeding into more users.

Forward Looking

Vulnerabilities

These flywheels that have served Zoom so well hint at two problems:

If it was so easy to attract users using some light differentiation, perhaps these same users would be easily attracted to a different service when the right alternative comes along. This could be because there's a technically better product (although the proprietary technology flywheel suggests this is unlikely), or that the definition of 'video conference' changes in an unpredictable way that Zoom is not ready for.

At a certain point the technology is simply good enough and/or a commodity. We're probably not there yet (or if we are, Zoom has exceeded the ‘good enough’ threshold), but it's conceivable that we will in the coming years. You could argue that, like flatscreen TVs, there will always be some new standard to reach for, but I have a hard time imagining users caring too much above a certain quality threshold.

Network Effect Vulnerabilities

I am not the first to suggest that Zoom has little in the way of a moat and is therefore vulnerable to upstarts. I think this is an overstatement: customers still need a reason to use a different service, and Zoom has a big lead in terms of video conferencing quality. I don’t imagine customers proactively seeking an alternative anytime soon.

The risk, then, is when the form factor of video conferencing ultimately changes. Video conferencing today is more or less indistinguishable from video conferencing 10 years ago, quality notwithstanding. I would argue no truly significant user experience innovation has taken place to make video chats feel more personal, more in-person. Fancy backgrounds and Together Mode notwithstanding, more often than not it’s just people staring into a camera, not making eye contact because they’re staring at their own faces, and hoping they can just communicate.

There are dozens if not hundreds of startups trying to iterate on the experience of video chatting itself. Just for one example, Miro is primarily a virtual whiteboarding tool, but they also offer in-app video chat for up to 25 people. Zoom could probably build a whiteboard feature in their app, but probably not as well as a whole team dedicated just to white boarding can (sound familiar?)

And really, the point is that Miro is just one of many possible directions video could go. If we assume that (1) we cannot predict which future iteration of video chatting will be most successful, but that at least one of them will be, and (2) that Zoom won't be able to build every possible one into its own app, then that suggests that Zoom is vulnerable to some kind of future innovation.

Proprietary Tech Vulnerabilities

I explained above why there may be a limit to how long Zoom can exploit the proprietary tech flywheel. When the time comes that the top competitors have matched Zoom on every parameter that customers really care about, what will happen then?

Yes, I already posited that customers may not have a strong reason to proactively seek a Zoom alternative. The big risk is that Zoom could lose users through inertia.

Zoom doesn't control distribution the way its competitors at Microsoft and Google do. Meetings tend to originate within an email or calendar app, and the largest email and calendar app companies—conveniently—have a video chat tool they’d love you to use.

Opportunities

So what's a Zoom to do in the face of these vulnerabilities?

Developer ecosystem

One of the risks I called out is future innovation undercutting Zoom’s existing customer base. Rather than pull a Facebook and either acquire or copy every nascent competitor, Zoom has an opportunity to create a robust developer ecosystem, allowing people to both build their own apps using Zoom’s core technology, or even more interestingly to build on top of Zoom to make Zoom itself more compelling.

Zoom has a major asset no startup can compete with—massive usage volume, each and every day. What if Miro, instead of building a competitor to Zoom with one distinguishing feature, could have built sold its whiteboard feature as an app inside of Zoom? That would likely have been a win-win for both sides, and allows Zoom to (1) stay relevant as technology changes, and (2) entrench customers with unique features.

[Note: there is an app marketplace and an API available on Zoom’s website today, but I think they are both half baked and barely scratching the surface of what they could be. Just as an example, it seems that the majority of apps in the marketplace are no more than ‘start a Zoom call from X’].

Reduce reliance on competitor distribution

If Zoom really is vulnerable to Microsoft and Google’s superior distribution, what could they do to change the equation? The straightforward answer is to counter by growing or acquiring distribution of their own.

To grow distribution, Zoom has already been adding new products like Zoom Phone that aim to expand their reach within a company’s communication stack. But I fear this won’t get them far enough fast enough, and that acquisition is the way to go. And specifically, I’d love to see Zoom acquire or merge with Slack.

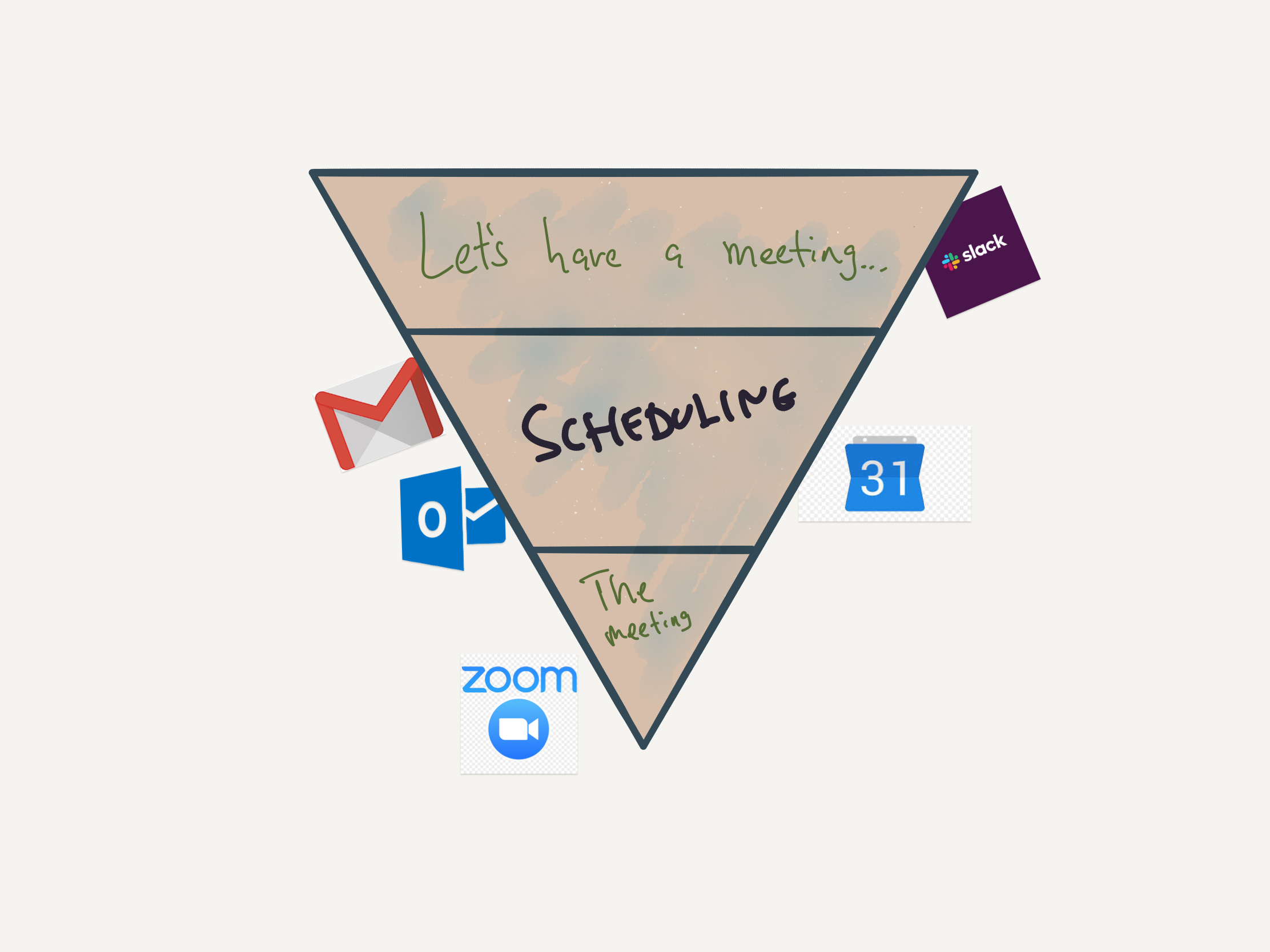

Slack is an actual, viable alternative way people schedule meetings outside of Outlook and G-Suite. In fact, it’s even high in the meeting funnel:

With Slack, Zoom could sidestep Google and Microsoft by meeting users at the point where they actually conceive of the meeting itself—in conversations with colleagues. And with a paltry $17B market cap, it’s basically pocket change for Zoom at this point.

That’s it for this edition of The Flywheel. Thanks so much for reading. If you liked this article, please subscribe and share with a friend!

And if I missed anything or you have any feedback, hit me up on Twitter or leave a comment.

Jake, really well done here. Its' interesting re-reading this analysis and then watching point solution competitors like HiPlatform go from $0 to $2b valuation in 18 months focused only on "large virtual conferences".

(something you allude to).

Keep these up. I hope you write more flywheel posts on SaaS companies!

Jake! This is fantastic content. You're a rockstar. It really made me think.

I think "good enough" is enough when it comes to chat communication, and that's why we saw Microsoft Teams eating Slacks lunch which forced their subsequent tie-up with Amazon. However, when it comes to video, which takes a lot more bandwidth, my thirst for better, more consistent quality is never satiated.

Btw, I love Facebook Portal is great but it didn't take off at all. I think Zoom could compete in the @ home hardware space. It's a crowded field, but at least they would own something rather than be vassals to the cloud providers.