DoorDash Delivers a Fairy-Tale Flywheel

Why DoorDash’s self-proclaimed flywheel is overly optimistic as we head into The Great Restaurant Renaissance.

Happy Thanksgiving to my US based subscribers 🦃! Welcome to the 158 new subscribers of The Flywheel. If you’re reading this but haven’t subscribed, click below to join 1,785 of your smartest friends and peers who receive The Flywheel in their inbox every other Tuesday.

Today I have a special shoutout: thank you to my very talented sister Jana Arbogast who helped me with the new branding you will have hopefully enjoyed.

If you liked this post, please click like and share with your friends! Onto the article.

Among the fun byproducts of writing The Flywheel is that people now send me flywheels. When someone sees a flywheel, has a question about a flywheel, or even just spins around inadvertently, I tend to hear about it.

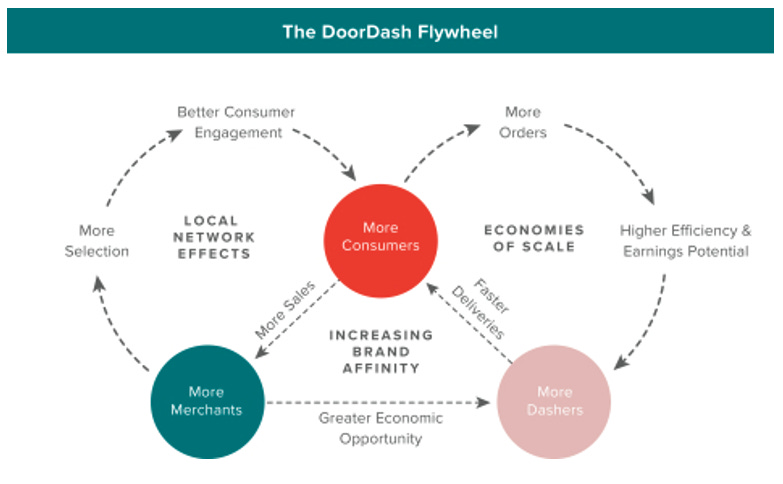

There is one flywheel that—in the words of the outgoing President—‘many people’ have been sending me lately. The self-published DoorDash flywheel:

This graphic was included near the top of DoorDash’s recent S-1 filing (the document that companies are required to publish when they intend to go public).

Given the rising prominence of DoorDash in our COVID-adjusted lives and the importance it has placed on its own flywheel, we’re going to do the first ever The Flywheel Flywheel Teardown, DoorDash edition. Order some dumplings and get comfortable, we’re diving in.

DoorDash’s Pitch to Investors

DoorDash is one of several companies that has filed to go public in the past month or so. In one form or another, many of these recent S-1 companies are attempting to strike while the iron is hot after a COVID boom. Notable examples include Airbnb, Wish, and Affirm (about whom I am writing in an upcoming S-1 Club report).

But perhaps none is demonstrating more opportunism than DoorDash, the food delivery company that is seeking to double its valuation to ~$30B when it hits the public market in the coming days, up from $16B just this past June.

DoorDash is intent on convincing investors that it is more than just a COVID story. The pitch is as follows:

We’re in a market leadership position today;

Overall market penetration is still low, even in the US; and,

We have a powerful flywheel that will help us extend our lead in the market, drive more penetration, and do all of this profitably.

This pitch is the clear story at the top of the S-1.

Market Leadership

DoorDash suggests that it’s gone from about one-sixth of the delivery market to one-half in 2.5 years. Notably, it has taken market share from GrubHub and ‘other’, which might be Amazon’s no-longer-existant Amazon Restaurants.

Low Delivery Penetration

DoorDash stresses that while it may have 50% market share, there’s plenty of room to run; after all, the addressable market for food delivery is pretty much all restaurant spend, or at least that which occurs ‘off premise’. From the S-1:

While we are the category leader, U.S. consumers on our platform in September 2020 represented less than six percent of the U.S. population as of September 30, 2020, and we believe we are in the early phases of broad market adoption.

In 2019, we generated gross order value on our Marketplace, or Marketplace GOV, of $8.0 billion. In the same period, $302.6 billion was spent off-premise at restaurants and other consumer foodservices in the United States.

Our Marketplace GOV in 2019 represented less than three percent of this off-premise spend, highlighting the large addressable opportunity ahead of us in the food vertical alone.

The Flywheel

No one will contest that food delivery is a large market opportunity. The more interesting debate is around DoorDash’s flywheel, because it is the tool it wants to use to convince investors that it has a unique opportunity in this space not only to continue to grow, but to do so profitably.

Profitability and Food Delivery

The question around food delivery companies has always been about profitability. Even as recently as March 2020 (incidentally right before COVID) the dominant narrative was that there just isn’t enough money to go around on a per-transaction basis. This NY Magazine piece does a good job explaining the problem:

I think the missing element for profitability is different: productivity. The hope with a lot of business models that bring app intermediation to a preexisting element of the economy like ride services or food delivery is that technology will make workers more productive. You can see instances where this is obviously true: a Peloton instructor who teaches a class to tens of thousands of people is more productive than a SoulCycle instructor who can only teach about 60 people at a time. But with a lot of apps, the promised boost to productivity never materializes. The worker still has to render personal service to one customer at a time, and the app doesn’t do much to reduce the worker’s downtime or help him or her complete the task faster.

If productivity and consumer willingness-to-pay aren’t increasing, then these firms must lose money—subsidized by massive VC rounds led by companies like Softbank—with the hopes that down the road...well, it was never clear what the long-term plan was. Perhaps it was to raise prices, but that’s always difficult in a competitive environment.

If this sounds familiar that’s because it is. It’s a tale as old as venture capital. This narrative was also one of the main undertones of the Uber-Lyft wars.

There has been exactly one quarter in DoorDash’s life that it has been profitable overall. But worse than that, it wasn’t until 2020 that it was net positive even on a contribution-profit—or per-transaction—basis. Contribution margin (i.e. the portion of an order’s value that flows to DoorDash) was below zero until Q1 2020. It was losing money on every order.

What’s changed in 2020 is that consumer willingness-to-pay has increased. In normal times, DoorDash, Uber (and others) would try to out-compete one another by offering progressively generous promotions. Since COVID, however, customers have been willing to tolerate larger delivery fees, higher menu markups, and—crucially—an absence of promotions.

The elimination of promotions was in large part responsible for the 2020 shift to contribution-profit positive. We can see this in DoorDash’s Sales & Marketing (S&M) Expense (largely promotions and discounts) as a percentage of Revenue figures, which decreased dramatically in 2020.

We can estimate what the impact would have been to contribution margin if S&M had stayed steady at the late 2019 level of 50%, a generous assumption considering that was already a large decline from earlier in 2019:

This would still show solid improvement, but it’s far from the story DoorDash is trying to tell. And that’s assuming that sales and marketing stays at the most DoorDash friendly pre-COVID level. If it went back to early 2019 levels, we would have an even more bearish picture.

Ever wonder where I get my public company data for these great looking charts? I use HyperCharts, a service that aggregates data for top public companies and presents them in a series of easy to consume charts. HyperCharts is great if you want to stay on top of the companies you’re analyzing or investing in. They’ve even added in all the new S-1 data from hot companies like Airbnb, Affirm, and yes, DoorDash.

If you use my link and eventually purchase a premium subscription, HyperCharts will share a portion of that revenue with me. It’s the best way to get information to inform your investing, and a fantastic way to support The Flywheel.

Why the Flywheel Matters

This is where the flywheel fits in. DoorDash wants to convince you that it has managed to flip the script—that it has unlocked the secret to delivering food profitably. That the bump it has seen in 2020 is sustainable. And it’s the flywheel, it says, that is responsible. Let’s take a deeper look.

Challenging DoorDash’s Flywheel

Let’s take another look at the flywheel image from DoorDash’s S-1:

DoorDash includes three unique but connected flywheels that are all related in some way to this question of profitability:

Network Effects

Economies of Scale

Brand

The argument appears to be that as DoorDash grows, (1) it establishes network effects that will make the platform stickier for both consumers and merchants, thereby providing pricing power to DoorDash. Additionally, (2) this will lead to greater economies of scale, i.e. ability to manage costs, and (3) an increasingly valuable brand that makes DoorDash the first company customers, merchants, and Dashers alike think about when they need to make decisions.

Let’s go through each piece:

Network Effects

Whether or not DoorDash has network effects depends on your definition of the term. The definition I prefer is similar to the one prominent VC firm a16z uses in its Network Effects presentation: “a network effect occurs when a product or a service becomes more valuable to its users as more people use it.” By that definition, you could argue that DoorDash has network effects, with the following blurb from the S-1 explaining why:

Local Network Effects: Our ability to attract more merchants, including local favorites and national brands, creates more selection in our Marketplace, driving more consumer engagement, and in turn, more sales for merchants on our platform. Our strong national merchant footprint enables us to launch new markets and quickly establish a critical mass of merchants and Dashers, driving strong consumer adoption.

But let’s look deeper. On the next slide, a16z says that network effects “create barriers to exit for existing users and barriers to entry for new companies (help build moats), protect software companies from competitors’ eating away at their margins, and can help create or tip winner-take-all markets”.

These criteria are a bit more challenging. DoorDash has zero barriers to exit for consumers, and perhaps only slightly stronger ones for merchants. Are there barriers to entry for new participants? Sort of. Restaurants are not locked in to one delivery partner, so in theory a new partner who delivers value can sign up restaurants even if they are signed up for DoorDash (and others) already. In fact DoorDash itself has proven this point by how ruthlessly it stole share from GrubHub.

At best, I’ll call DoorDash’s network effect weak or indirect. Yes, merchants want to join platforms that more users are on, and users want to join the platform where the merchants are. But the intent of network effects is to demonstrate a strong strategic position, and I don’t believe we can conclude it has one from DoorDash’s network effect.

The indirectness of the network effect presents problems on both the merchant and consumer side. For merchants, it’s not clear if more orders actually lead to more merchants signing up. It is equally plausible that merchants sign up for DoorDash because they sign up for every reasonably large delivery company. For a merchant you don’t only want to be on the #1 delivery service, you want to be everywhere customers might look.

For consumers, the network effects are even weaker. The classic example of a consumer network effect is a social site like Twitter, where the fact that other people are using it makes me want to use it, and as that grows it makes me more unlikely to churn. There is no such dynamic for DoorDash. All DoorDash can offer consumers is selection, but the selection is not unique. It takes almost zero effort to price compare between DoorDash and Uber Eats.

Economies of Scale

From the S-1:

Economies of Scale: As more consumers join our local logistics platform and their engagement increases, our entire platform benefits from higher order volume, which means more revenue for local businesses and more opportunities for Dashers to work and increase their earnings. This, in turn, attracts Dashers to our local logistics platform, which allows for faster and more efficient fulfillment of orders for consumers.

DoorDash expects its unit economics to improve with more scale. More orders lead to more merchants lead to more dashers. The density of the network increases, which means delivery times will decrease, which will lead to more orders, and so forth.

Indeed, DoorDash could improve efficiencies. For example, the more data it collects, the less time it might have Dashers hanging out at restaurants waiting for food to be ready. There are a bunch of different ways it could shave a minute or two off delivery times.

The bigger opportunities to improve efficiency are those that improve capacity utilization, such as the following:

Batch orders together. Perhaps like UberPool, a customer might pay a little less to have their food arrive a little slower. In fact Uber already does this to some extent. The problem with this idea is that food needs to be delivered hot and quickly. There is a low upper-limit to how many food deliveries can be batched together before people get angry.

Give Dashers a way to continue making money even when order volume is low (say, in between meal times). DoorDash is expanding into services like grocery, for example, to address this opportunity. The problem here is that it is at a disadvantage compared to competitors, in particular Uber which has an entire, separate business to which to shift drivers when UberEats volume is low.

DoorDash wants us to believe that as it grows, its economics will become better than anyone else’s. Its economics may improve, but I don’t see any special advantage DoorDash has here. Perhaps if it merged with someone like, say, Lyft, it could be in the conversation with Uber on this topic.

Brand

Again, from the S-1:

Increasing Brand Affinity: Both our local network effects and economies of scale lead to more merchants, consumers, and Dashers that utilize our local logistics platform. As we scale, we continue to invest in improving our offerings for merchants, selection, experience, and value for consumers, and earnings opportunities for Dashers. By improving the benefits of our local logistics platform for each of our three constituencies, our network continues to grow and we benefit from increased brand awareness and positive brand affinity. With increased brand affinity, we expect that we will enjoy lower acquisition costs for all three constituencies in the long term.

I could be convinced that DoorDash has strong, if indirect, network effects, and has the opportunity to improve its unit economics, at least to a point. But that DoorDash has strong and increasing brand affinity that will decrease acquisition costs and improve retention? Not so fast.

The truth is that not one of the three constituents cares much about DoorDash the brand.

Dashers don’t particularly care about DoorDash the brand. They will go to whomever is offering the best rates and the highest tips. It’s a transactional relationship, and drivers may even deliver for multiple apps at the same time.

Merchants don’t care about DoorDash the brand. In fact they are more likely to feel that delivery services are eating their lunch. I’d love to see data on the median number of delivery partners restaurants are signed up with. I am sure it’s closer to 5 than to 1. An admittedly unscientific casual survey of mine and Tanya’s 5 favorite DC takeout places show that 4/5 are available on both DoorDash and UberEats.

Consumers really don’t care about DoorDash the brand. DoorDash doesn’t provide the end product to customers, the restaurant does. They care a lot about the brand of said restaurant and the price they have to pay. They are happy to switch to another service if they can save a couple of bucks. That is not the hallmark of a strong brand.

DoorDash wants us to believe that because of its brand, it will be able to charge merchants and consumers higher fees, and/or pay Dashers less. But in reality, DoorDash has limited ability to lock in any one of its three constituents.

DoorDash has tried locking in consumers, for example, with a $10/month subscription called DashPass, and apparently it has 5 million users signed up so far. Unfortunately the S-1 doesn’t break out how many of these users are actually paying for it, versus it being provided for free by Chase Sapphire.

From personal experience, even with my DashPass subscription, I price compare and ultimately order frequently from UberEats.

COVID and Food Delivery

We’ve gone through the flywheel and why I am highly skeptical that DoorDash has built or could build unique advantages. But what about COVID? Maybe the shift I described above is here to stay?

After all, we’ve seen a similar story with Peloton and Zoom, where the world shifted to ‘at-home’ fitness and meetings and realized that it’s actually a pretty good stand-in for the real thing. In those cases, I believe the COVID bump is sustainable, and clearly the stock market agrees.

So why not DoorDash? The answer is simple: unlike with exercise or work, people haven’t suddenly shifted to delivery and realized, ‘you know what, this is just as good as eating at a restaurant”. In fact, it’s just the opposite. The moment it’s safe to do so, we’re going to see an unprecedented restaurant bonanza.

When that happens, we’re likely to see the following: DoorDash, UberEats, and the others will resume their cutthroat price wars. Consumers will return to their deal surfing practices. DoorDash will be forced to once again spend 50%+ of its revenue on sales and marketing, and will therefore return to negative contribution margin territory.

Final Thoughts

To DoorDash’s credit, it calls out the unsustainable nature of its super-high growth rates in 2020: “The circumstances that have accelerated the growth of our business stemming from the effects of the COVID-19 pandemic may not continue in the future, and we expect the growth rates in revenue, Total Orders, and Marketplace GOV to decline in future periods.” Indeed, DoorDash, they may not continue.

But what it doesn’t say is that it would never have filed an S-1 if not for COVID. Instead, it attempts to convince investors that it has figured out some trick to delivering food profitably, something that eluded them until this year:

Our historical consumer cohorts demonstrate attractive and improving financial results because we have been able to retain and grow consumer demand while normalizing sales and marketing and promotions spend.

In other words, ‘we know we used to have to offer huge discounts to people to use our platform before, but that’s in the past now’.

I don’t think that it is. My sense is we will circle back to the narrative that this market—the one that Amazon decided to get out of after years of trying—is one that simply does not support venture-scale outcomes.

That’s it for this edition of The Flywheel. Thanks so much for reading. A huge thanks to Tanya, Mom, and Abe for helping out with this one.

If you’re looking for something else to read this week, check out Visible Hands. I enjoyed their recent primer on carbon pledges and what it means for a company to make one.

If you liked this article, smash that like button and share with a friend! Let me know your take on Twitter here.